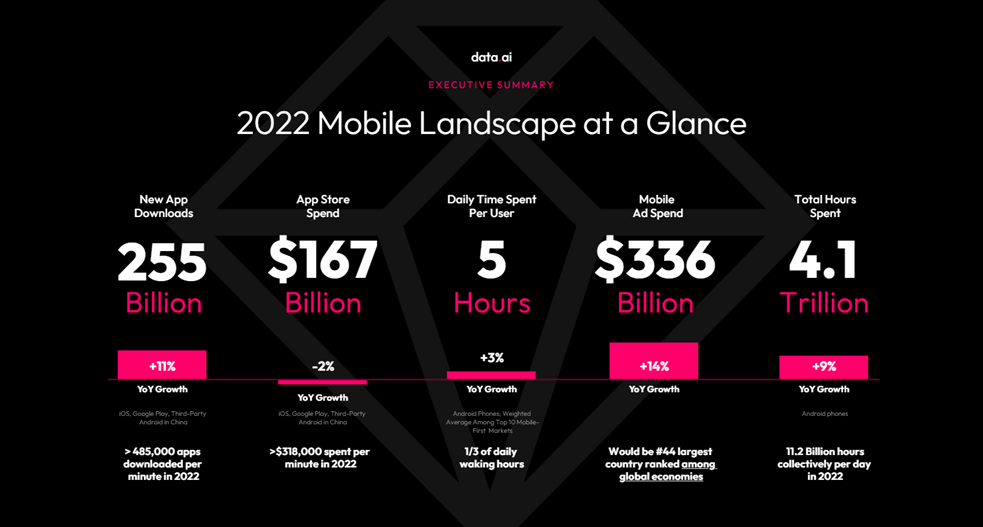

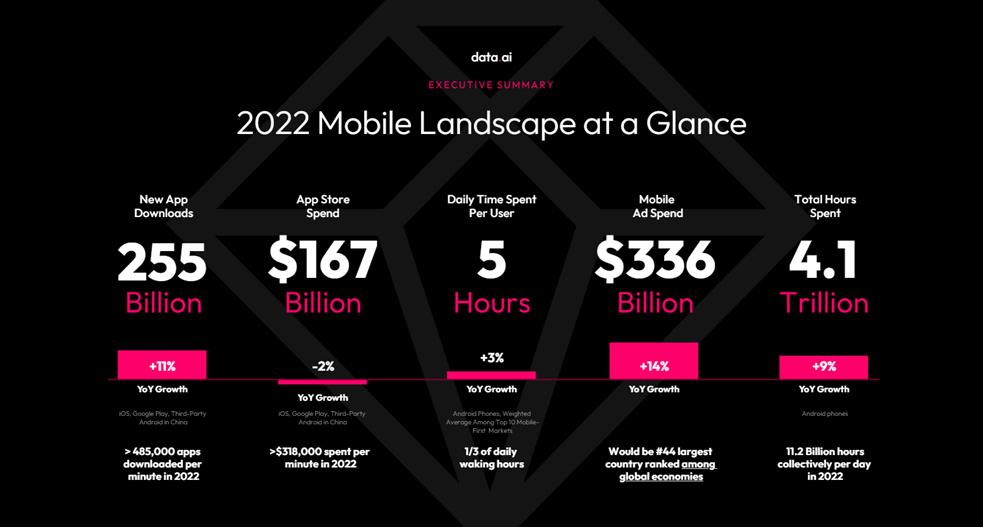

data.ai (formerly App Annie), reveals in its annual State of Mobile 2023 Report that demand for mobile apps accelerated last year while consumer spend shrank. Downloads grew to 255 billion (+11 per cent YoY), and hours spent peaked at 4.1 trillion (+9per cent YoY). Meanwhile, consumer spending across all app stores, including third-party Android marketplaces in China, slipped by 2per cent YoY to $167 billion as economic headwinds impact discretionary spending. The most downloaded game in India is Ludo King, according to the rankings.

“For the first time, macroeconomic factors are dampening growth in mobile spend.Consumer spend is tightening while demand for mobile is the gold standard. In 2023, mobile will be the primary battleground for unprecedented consumer touch, engagement and loyalty,” says data.ai chief executive officer Theodore Krantz .

Short-Form Video apps, led by TikTok, dominated consumer attention in 2022. Users of these apps streamed a whopping 3.1 billion hours of user-generated content daily, up 22per cent YoY, and spent $5.6 billion, up 55per cent YoY, fueling the creator economy.

More key findings include:

- Time spent on mobile increased to 5 hours per day, up 3 per cent YoY in the top 10 markets.

• OTT (Over-The-Top) apps such as Netflix and Disney+ grew 12per cent YoY to $7.2 billion.

• Mobile ad spend is set to hit $362 billion in 2023, driven by growth in short-form video and video-sharing apps like TikTok and YouTube. - Spending on gaming apps dropped by 5per cent YoY to $110 billion, yet downloads reached new records at 90 billion, up 8per cent YoY.

- Spending on other apps (non-gaming) increased by 6per cent YoY to $58 billion, largely driven by subscriptions and purchases in OTT, dating, and short videos. Downloads increased 13per cent YoY to 165 billion.

- Simulation game genres, including Simulation Driving, Hypercasual Simulation, and Simulation Sports, drove growth YoY for downloads, while Action MOBA and Roguelike ARPG games bucked the spending downturn.

- Financial volatility reshaped consumer appetite for risk: in the US, crypto trading and investing app downloads dropped 55per cent YoY, while personal loan app downloads surged 81per cent. Price-sensitivity reshaped consumer retail spending priorities: BNPL (Buy Now, Pay Later) app downloads grew +47per cent YoY, Coupons & Rewards +27per cent, and Budget & Expense Tracker +19per cent.

- Rebounds in travel and interest in language learning command share of wallet despite tightening purse strings. Apps such as Booking.com, Airbnb, and Duolingo saw growth.

- 1419 apps and games generated over $10 Million dollars annually in 2022.

- Decline in spending disproportionately impacted top games: While games represent over 60per cent of apps in all measures, they were also the most affected by cooling consumer spend. The number of games surpassing $10M, $100M and $1B spend dropped by -1per cent, -4per cent, -33per cent YoY respectively.

- In 2022, well known IP games such as Diablo Immortal and Apex Legends Mobile saw success in adoption and IAP consumer spend as mobile games are now capable of offering console-like graphics and gameplay experiences.Hit Open World RPG Genshin Impact continues to break new grounds, crossing its $3 Billion in IAP Spend in Q2 2022.

- Hypercasual games like Merge & Fight and DOP4: Draw One Part were key downloads driver, but 2022 saw some surprise hits such as Party Royale Game Stumble Guys, and Word Puzzle Game Wordle, making major gains in downloads and usage.

- Consumer spending on RPG games is the largest, totaling $25 billion for in-app purchases.

- Hyper casual games has the highest number of downloads with 17.5 billion downloads.

- Creative Sandbox games such as Roblox and Minecraft dominate growth in many markets — Globally, time spent grew 25 Per cent from 2021 to 2022. In South Korea, usage in Creative Sandbox games grew by over 45 per cent year-over-year.Conversely, Battle Royale (Shooting) games were among the biggest ‘losers’ of 2022 — seeing time spent decline by around 20per cent globally.

- Markets that buck the trend include China and Saudi Arabia, where Battle Royale Games grew boomed +15per cent and 45per cent, respectively.

- Younger gamers gravitate towards party, simulation and shooters; match 3, slots and puzzle preferred by older age groups

- Match 3 and puzzle games tend to skew towards female audience, while sports, strategy and shooting skew male

- Top 10 games in India in terms number of downloads are as follows- Ludo King, FreeFire, Carrom Pool, Candy Crush Saga, Subway Surfers, Subway Princess Runners, Temple Run, Bridge Race, Hill Climb Racing, Shoot bubbles Pop bubbles.

This year’s State of Mobile report identifies and discusses macro-trends for leading brands and publishers and what success looks like for mature apps across gaming, fintech, retail, social, video streaming, and more. The report delves deep into demographics and app, and game categories made possible by the more than 250,000 apps categorised under data.ai’s industry-first Game and App IQ taxonomy.